Most people wait for something bad to happen before taking action. Why? Something bad happening in your life reminds you of how precious life is. This reminder is what helps you to remember to take action.

This past Sunday, 1/26/20, will go down as a historic day in history. We lost one of the greatest athletes of all time, Kobe Bryant. There were also 8 other victims in this horrible helicopter crash.

I was on a flight from MCO to San Francisco when the news broke. I landed in San Francisco to a text from a friend saying “RIP Kobe”. Naturally, the first thing that comes to mind was Kobe was probably in the news for losing a 1v1 in basketball or something to that extent. I got curious, so I went to google and put in his name. I was devastated at the news I saw. I couldn’t believe what I was looking at. There was no way the news could be real. To say I was shocked is an understatement.

We are all on different parts of our journey. No two people are alike. No two people will agree on everything. Don’t let any of this make you miss out on living every day with purpose. You never know what could happen. The world isn’t always fair.

Here is one thing I would love for people to take away from this tragic event. Stop waiting.

Stop waiting for something bad to happen in your life before you want to change.

Stop waiting for a New Year to come around where you will then magically change.

Stop waiting to tell the people you care about that you care about them.

Stop waiting to repair that relationship that is long overdue.

Stop waiting to take control of your life and your path to financial independence.

Stop waiting for your actions to match your words. Talk the talk and walk the walk.

Third and final core principle. House hacking is by far the most powerful way to begin your investing journey. When you think about getting ahead in your investment journey, eliminating your largest expense by house hacking becomes powerful. For 99% of people, the largest monthly expense you have is housing. If you are able to eliminate your largest expense by house hacking, you will put yourself in a position to aggressively save.

What Is House Hacking?

Let’s first answer what house hacking is. I go into much further detail on house hacking and different ways to house hack in this previous post. In the most simple terms, house hacking refers to purchasing a single family or multi family home and renting out portions of it. There are many different strategies to go about doing this, but the concept is to reduce your living expenses. The best house hackers are able to live for free or even make a little bit of money from their home.

Common Excuses to Not House Hack

What are the most common excuses I receive when I tell people that I house hack?

I have a family and wouldn’t feel comfortable house hacking.

Renting is just more simple and I don’t want to deal with a home.

I enjoy living on my own and don’t want to live with others.

Roommates? Yeah, I graduated from college already and I am a grown adult. I want my independence.

I don’t have the money to buy a home.

I don’t make enough to buy a home right now.

Cool, so what I hear is you have a fixed and limited mindset. Awesome. Just make sure you are aware that all the above excuses are those of people having a fixed mindset. These are all excusesand not valid.

Have a family and don’t think it is safe? Buy a multi-family property and you will have your own space. Even a single family home with a detached 1/1 unit would do.

Don’t have the money? Money is abundant and available these days. Stop making this excuse. If you had to raise $20,000 tomorrow to get in a deal that could pay off hundreds of thousands of dollars, would you be able to get the money? It isn’t the fact that you don’t have money, it is that it’s easier to make this excuse.

I don’t make enough money. Interesting, did you know lenders can help qualify you for a loan with the rental income counted as part of your income? Stop with the fixed mindset.

Why Is House Hacking A Core Principle

House hacking is a core principle because I simply don’t see why you wouldn’t do it. It makes too much sense to do. There are many different ways to effectively house hack. Any and all excuses you could have for not house hacking are just that, excuses.

I wish I knew about house hacking even when going to college. I would have bought a property in Buffalo, Arkansas and then Bethlehem, PA when I lived in each. Now that I have learned and successfully house hacked my first property, it is time for more.

How Am I Currently House Hacking

Want to hear the full story about how I got started house hacking? Checkout my recent podcast I was interviewed on where I speak about exactly this.

When I moved to Florida, I purchased a single family home in a nice area. I had no intention of house hacking at the time because I had never heard of it. I knew I wanted to buy a home versus renting an apartment. I was tired of paying someone else’s mortgage. I stumbled into house hacking when a friend of mine asked to come down for a few months. From there, I took it and ran with it.

My current house hacking strategy is renting out by the bedroom. I live in the master bedroom in my home and have three other bedrooms I rent out to young professionals living in the area. I bring in $2,400 per month in rent on a mortgage of $1,650. After all expenses, I typically make $100-200 per month. That is right, I get paid for the privilege of living in my own home!

My Next House Hack – Changing My House Hacking Strategy

For my second house hack, I plan to leverage a different strategy. I am planning to buy a multi-family property where one of the units is a 1/1. The goal is to get one of the following:

Single family home with a detached 1/1 unit

Duplex with one unit being a 1/1

Triplex of any kind with one unit being a 1/1

This next house hack will be a big step in my continued venture in investing in my financial independence. I am excited for the next steps in my journey and hope you seriously look into house hacking.

Key Takeaways:

Your largest expense is typically housing. For that reason, you should look to eliminate your largest expense by house hacking!

Stop making excuses on why you can’t house hack. I can find a reason why every excuse is not valid.

There are many strategies. Each can be used depending on your life situation and market you live in. Don’t think there is only one way to do this successfully.

If you haven’t already, below are links to my first two core principles.

The ability to understand your expenses when analyzing a short term rental investment is critical. Income is only one side of the equation. If you are able to effectively understand your expenses, you will be able to put together projected cash flow numbers. This will help you determine if a property is worth investing in.

Before reading this article, if you haven’t already checked out my Understanding the Inputs post, start here. This post will help you understand some critical inputs you will need for effectively analyzing the income side of the equation for short term rentals.

The Two Main Ways to Get A Short Term Rental Property

When looking to understand what expenses come with short term rentals, there are two main ways people get a property. These are the common purchase of a property or master leasing.

Purchasing a property is pretty straight forward. The main downside of purchasing a property is capital. Purchasing properties will take more cash to get started. There are a significant number of benefits to purchasing. I won’t go into the details in this article, but you can read through some pros and cons of purchasing a home here.

The second common practice used is master leasing a property. What is master leasing? When you master lease a property, you are signing an agreement with the landlord allowing you rights to sub-lease. To learn many more intricate details of how master leasing works, you can go here.

You would be able to sublease the property for the duration of the signed lease. One thing I want to make clear on my viewpoint of master leasing. Master leasing can be a great option for someone with less capital. If this is a strategy you would like like to implement, make sure you provide full transparency to the landlord. Let them know your intention of what you plan to do with the property. I believe it is unethical to not be honest with any landlord you are trying to master lease with. Ensure to tell them your exact intentions with the property.

Okay, now that we got that part out of the way, let’s get into how to understand your expenses for both scenarios. Before jumping in, to clarify, this is how I run my numbers. This is not the only way to run the numbers for a short term rental. This is how I run the numbers when analyzing short term rental investment properties.

Understanding Your Expenses – Common Expenses

Below are the common expenses you will have for your property regardless of buying or master leasing:

Utilities: this will be any utility costs associated to the property. Typically, this will include cable, internet, electric, heat, and water.

Misc. Expenses: This category was put in the analysis so you can add extra expenses for one off scenarios. I don’t want to clutter the template with line items for too much. If you have a miscellaneous expense, put that here. An example of this type of expense is pool maintenance. I currently pay $90/month for a pool guy to service my property.

Understanding Your Expenses – Purchasing a Property

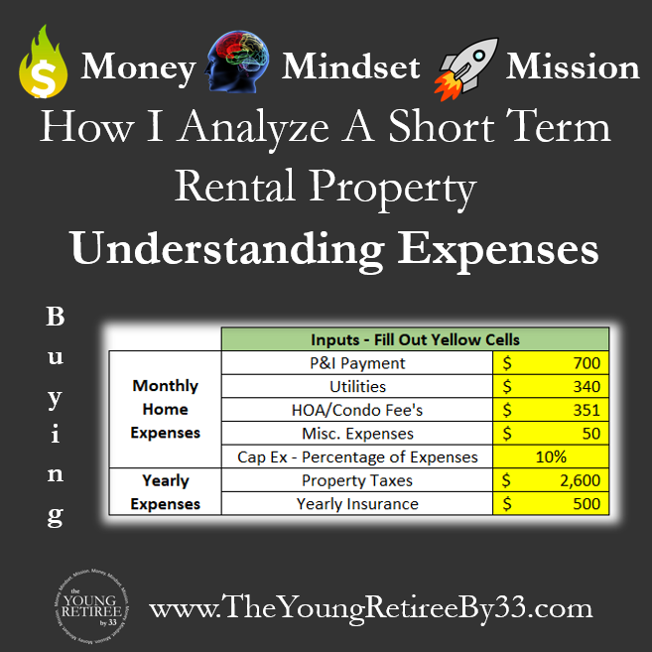

The most common thing for real estate investors to do. Let’s look at a snapshot of the different expenses it is important to understand:

As the owner of a property, you will incur more expense lines than if you were renting. This is natural based on the nature of how you are operating the property.

Let’s first touch on the expenses that will be different from master leasing. These include: Principal & Interest Payment (P&I), HOA/Condo Fees, Capital Expenses, Property Taxes, and Yearly Insurance.

What is P&I? This is your principal and interest payment. When purchasing a property, you will have loan terms and an interest rate. These to things will help determine what your principal and interest payments are each month.

What are HOA/Condo Fees? When you are an owner of a property, you must make sure you account for HOA/Condo Fees. These aren’t common in all parts of the country, but you need to factor this in. High HOA or Condo Fees can very quickly turn what you thought was a good investment to a bad one. For example, my property in Orlando has an HOA fee of $351 per month. I am more than happy to pay this for a few reasons. The HOA takes care of the exterior of the entire home including lawn maintenance. This fee also includes free access to my guests to all amenities within the resort. I made sure to factor this cost into my analysis before purchasing.

What are Capital Expenses? Capital expenses are the larger expenses like a new roof, remodeling kitchens, painting the exterior, replacing an AC. These are some of the most common capital expenses but not the only ones. Each month, you want to put away a percentage of your income to the side. This will be used when you have one of these larger expenses pop up. For example, earlier this month, I received a text from my pool guy letting me know the pool pump needed to replacement. This would is a capital expense and ended up costing me $2,400. That is part of the business, so don’t forget to account for this in running your numbers! I currently use 10% for this when running my numbers. Why? I have generally heard that is how much you should put away for capital expenses. So that is what I do. No crazy analysis for that one.

What are property taxes? Uncle Sam will always want his fair share. Part of owning a property is paying property taxes. If you are looking at properties on the MLS, you should be able to see the most recent tax year bill. One thing to be careful about. Property taxes typically increase over time. This will change every year based off new assessments made by the government.

What is yearly insurance? This is just your normal yearly insurance on a property. To get a good estimate, call some insurance providers in your area and talk through property characteristics. This will help you ballpark this number. For all your numbers, it is always good to be a little conservative. This will only help you in the long run. As you get a few properties, you will be able to dial in these numbers to become more accurate.

Understanding Your Expenses – Renting or Master Leasing A Property

When renting or master leasing a property, the below expenses will need to be defined:

Rent: This is pretty straightforward, but this will be the monthly rent payment for the home.

Operational Expenses: If you would like to add extra operational expenses per month, I have added a line to do so.

Key Takeaways:

There are two main ways to get a short term rental property. You can buy a property or master lease.

Doing either of these strategies will change how to properly analyze the property. Understand what is necessary to use for either purchasing or master leasing

Whenever you plug in numbers, do as much research as possible to closely approximate costs. When in doubt, always overestimate expenses so your numbers are conservative.